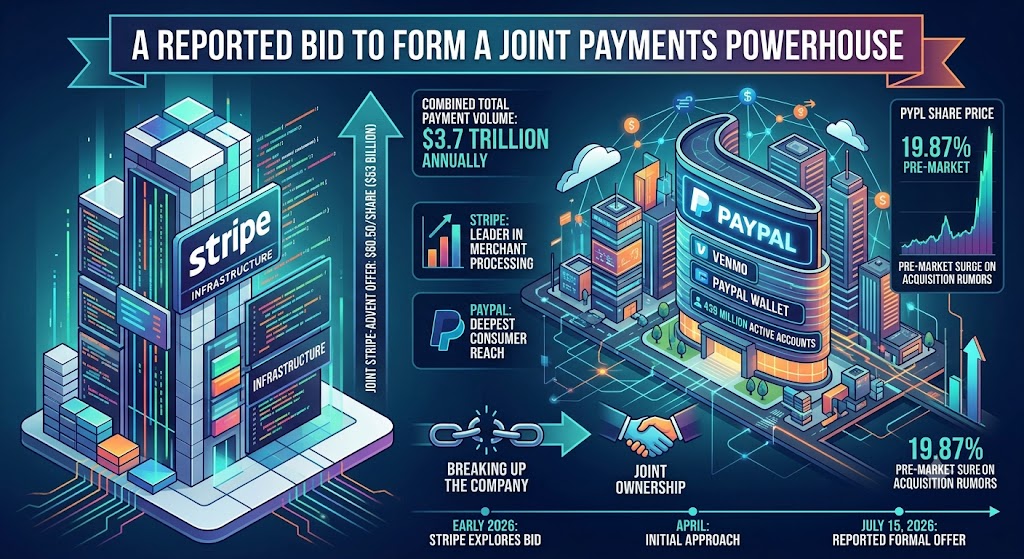

Payments giant PayPal is the target, not the buyer, in one of the biggest fintech stories of the year. Stripe and private equity firm Advent International have made a joint offer to acquire PayPal Holdings for $60.50 a share, in a deal that would value the company at more than $53 billion. The bid represents roughly a 28 percent premium to PayPal's closing share price on Tuesday, July 14, and shares of PayPal closed 17% higher on the news.

Under the proposed structure, Stripe and Advent would jointly own PayPal, with each holding an equal stake, rather than breaking the company apart or absorbing it into Stripe's existing business. Stripe, Advent and Block are reportedly contributing $17 billion in equity to the offer, which also includes roughly $50 billion in committed bank financing. The offer was submitted earlier this month and follows an initial approach made in early April, and PayPal's board is expected to meet as soon as July 20 to discuss it. Crucially, nothing is settled: there is no certainty the approach will result in a completed transaction, and PayPal has been working with Goldman Sachs and Evercore to review strategic options, including a potential sale or breakup.

Why now?

The bid lands at a low point for PayPal. PayPal stock is down 18% year to date and 35% lower than one year ago as competition from Apple Pay, Block, Stripe, and buy now, pay later firms like Affirm and Klarna has crowded the market. The company issued disappointing profit guidance for 2026 and replaced former CEO Alex Chriss with HP's Enrique Lores as its new president and CEO. Stripe, meanwhile, is riding high: it was valued at $159 billion in a February 2026 tender offer, a roughly 70 percent increase from its valuation a year earlier, and processed nearly $1.9 trillion in total payment volume in 2025, up 34 percent from the prior year.

Not everyone thinks the price is even right. Investor Michael Burry, who holds PayPal stock, has argued the offer undervalues the company and suggested any successful bid would need to go higher. Add in the likelihood of serious antitrust scrutiny for a merger of two of the world's largest payment processors, and this looks like the opening move in a long negotiation rather than a done deal.

What it could mean for fees

If a Stripe-PayPal tie-up did eventually close, the fee picture for SMEs is genuinely mixed, not straightforwardly bad or good.

On one hand, consolidating two of the biggest names in payments reduces the number of major players at the top of the market, and reduced competition at that level doesn't typically pressure prices downward. Integration costs on a deal this size (tens of billions in financing) would also need recouping somehow, and merchant fees are an obvious lever.

On the other hand, PayPal has been losing ground precisely because rivals like Apple Pay, Block, Klarna and Affirm have been undercutting it on price and experience. That competitive pressure doesn't disappear if Stripe and PayPal combine. There's also a plausible upside case: Stripe's developer-first infrastructure paired with PayPal's enormous consumer wallet base could let a combined company offer more efficient, bundled pricing for merchants who currently juggle both a checkout provider and a wallet/BNPL option separately.

For now, nothing changes. No fee revisions have been reported, and any restructuring would be a long way off even in the fastest-moving scenario.

What it could mean for customer service

This is where SMEs should probably pay closer attention. Large-scale fintech mergers tend to create real friction during integration: account migrations, API and webhook changes, support ticket backlogs, and shifting points of contact as teams get merged or made redundant. Stripe and PayPal have quite different product philosophies, Stripe built around developer tooling and API flexibility, PayPal built around a mass-market consumer wallet and checkout experience, and reconciling those into one coherent product roadmap is not a quick job.

Businesses that rely heavily on either platform's specific tooling (custom Stripe integrations, or PayPal's dispute resolution and buyer protection flows) should expect that a completed merger would eventually mean some consolidation of features, possibly to the benefit of merchants long-term, but with a bumpy transition period in the middle.

What SME owners should actually do

- Don't rush to migrate providers. The deal hasn't been accepted by PayPal's board, and deals of this size can take many months to close, if they close at all, given the regulatory scrutiny involved.

- Check your existing contracts. Know your notice periods and any early termination costs before considering a switch.

- Keep a secondary payment option evaluated, even if you don't act on it yet. It's cheap insurance against disruption.

- Follow official statements, not headlines. Coverage on a story like this moves fast and details (price, structure, timing) are still shifting.

The honest summary: this is a live, contested takeover bid, not a completed acquisition, and it's Stripe pursuing PayPal rather than the reverse. For SME owners, the sensible move right now is to watch closely and plan contingencies, rather than react to a deal that may still be months (or years) from resolving one way or the other.

Stripe's Bid for PayPal: What It Could Mean for SME Owners